Thailand

Thailand

Vietnam: VND depreciation pressures predicted to be less pronounced in 2019: HSBC

The Hanoitimes – Despite global growth slowdown in 2019, Vietnam is expected to grow at 6.5% year-on-year whereas inflationary pressures are likely to remain benign and well below the State Bank of Vietnam’s (SBV)`s 4% ceiling at 3.4% year-on-year.

In its recent report, British bank HSBC expected depreciation pressures on the Vietnamese dong (VND) to be less pronounced than in 2018 and adjusted its forecast for the USD/VND rate to VND23,550 (from VND23,800 earlier).

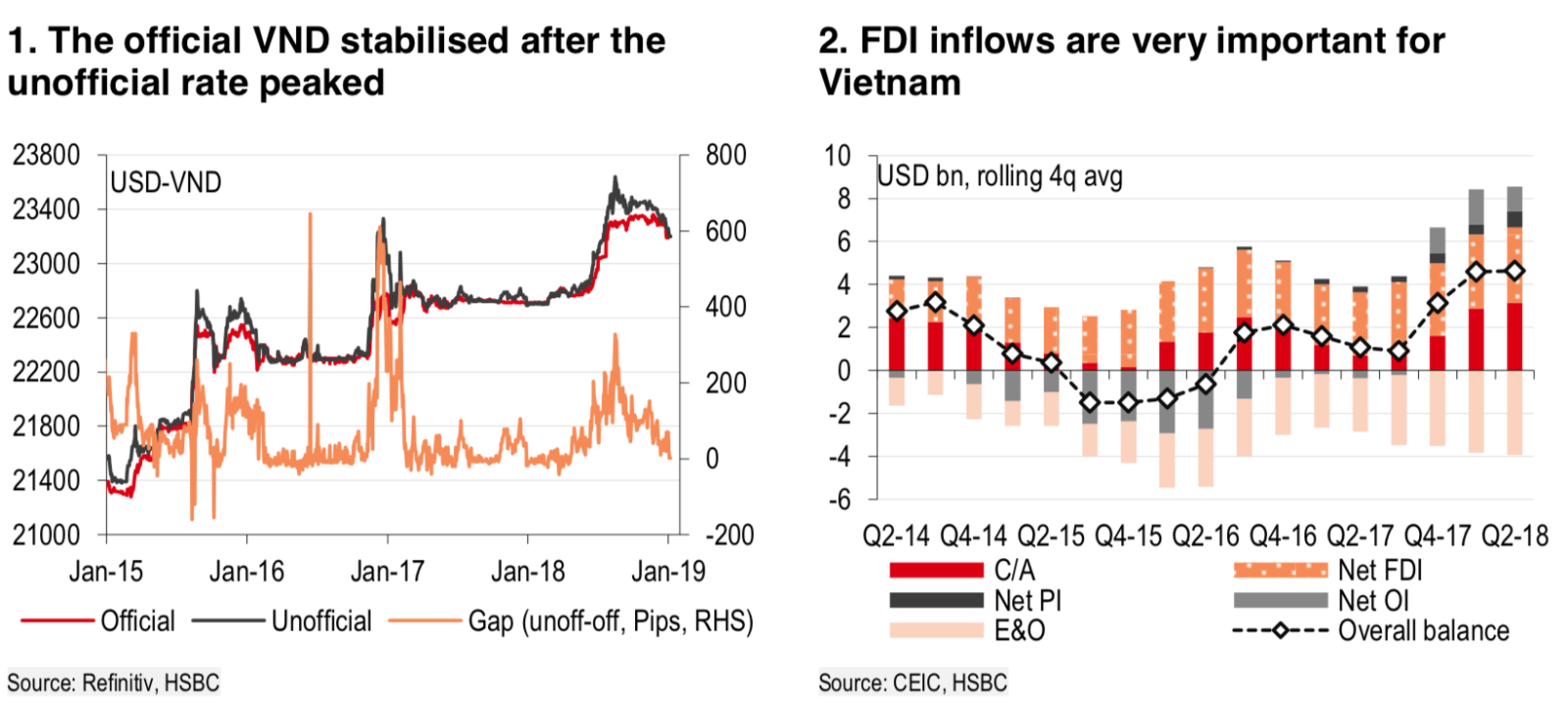

In 2018, the VND faced greater depreciation pressures from a weaker renminbi (RMB), heightened trade tensions between the US and China, and a stronger US dollar (USD). The depreciation pressures can be seen in the divergence between the unofficial and official VND exchange rates – with the former trading above the latter for most of 2018.

However, this gap narrowed considerably after the RMB depreciation concerns subsided, stated HSBC.

External pressures have probably also been tempered by the VND’s relatively solid fundamentals. Growth has been strong at 7.08% year-on-year in 2018 and inflation has been reasonable at 3.5% year-on-year on an average basis.

Despite global growth slowdown in 2019, Vietnam is expected to grow at 6.5% year-on-year whereas inflationary pressures are likely to remain benign and well below the State Bank of Vietnam’s (SBV)’s 4% ceiling at 3.4% year-on-year.

Meanwhile, Vietnam’s trade surplus rose to a record-high US$7.7 billion in 2018, US$5.6 billion more than in 2017, according to HSBC data. The trade outlook in 2019 should be supported by the implementations of the Comprehensive and Progressive for Trans-Pacific Partnership (CPTPP) and the EU-Vietnam FTA.

As for the capital account, the report noted that Vietnam’s equity market is the only one in the region (other than China) that received net inflows of US$1.9 billion in 2018. Additionally, realized FDI inflows in 2018 was estimated at US$19.1 billion, up by 9.1% over 2017. Registered FDI had also shown signs of recovering in the final month of 2018. FDI is the primary source of capital inflows for Vietnam that helps the central bank build FX reserves.

The uncertainties in US- China trade relations should accelerate the diversification of manufacturing production capacity from China to Vietnam. For example, China’s GoerTek, which assembles wireless earphones for Apple, lately suggested it intends to relocate some of its production to Vietnam.

Additionally, a degree of stability in the VND is also important for foreign enterprises managing FX translation risks and planning future investments. The authorities have prudently stabilized the VND, even if it has meant FX reserves dipping to US$60 billion as of October 2018. That said, net reserves were still up by US$6 billion in 2018.

It is expected that FX reserves could increase further in 2019. On January 2, the SBV raised its USD buying rate to VND23,200 (from VND22,700 earlier) and signaled its willingness to mop up foreign inflows.