Thailand

Thailand

Vietnam: How the central bank can get to grips with dipping rates and economic turbulence

As global central banks begin to neutralise loosened monetary policy, such as the Fed lowering rates, this is seen as positive signals as the world economy gradually recovers, minimising the risk of global economic crisis.

Looking into the past, even in the period when the Fed raised interest rates at the end of 2015, the negative and direct impacts on Vietnam are not always clear.

Interest rates on government bonds since 2015 as well as interest rates in the economy have logged in a downward trend; exchange rate maintained a steady decrease of approximately 2 per cent per year. Furthermore, foreign direct investment registered and disbursed inflows have maintained at a steady pace.

From the perspective of a highly open economy, the top priority is to ensure macroeconomic stability and create attractiveness for international investment inflows. Accordingly, Vietnam may use resources and foreign inflows to boost production, raise income per capita, and escape the middle-income trap.

This mission has been successful over the years. With the assumption that Vietnam will contain the pandemic and maintain good macroeconomic indicators, investment capital flows may reach Vietnam based on the country’s risk level and potential growth of the economy. This is also the same assessment as credit rating agencies currently give Vietnam.

Thus, in the long term, when the monetary policies of the central banks gradually make the easing phase come to an end, Vietnam still has the conditions and resources to ensure macroeconomic stability. In particular, the trend is shifting towards investment flows from China (and other countries) to Vietnam. At the same time, free trade agreements are also helping Vietnam to attract more international funds.

In the short term, compared with other central banks in the world, the State Bank of Vietnam (SBV) only lowers operating interest rates and has no plan to buy back assets such as bonds. Thus, this is considered a good point in terms of flexibility in monetary policy.

Along with that, another plus point is that the appropriate management policies have shown their effectiveness in stabilising macroeconomic indicators such as exchange rate, inflation, or interest rates in different sectors in recent years.

However, some challenges for the SBV in 2021 come from increasing pressure from the large openness of the economy. Import and export turnover tends to increase relative to the size of the economy given that raw material prices are high, creating pressure on controlling inflation. Moreover, the SBV might find it hard to balance the great pressure on harmonising the interests of depositors and borrowers.

Last but not least, it would have to deal with how to better support businesses recovering after the pandemic, but also need to minimise capital inflows into risky assets such as real estate speculation.

Basically, monetary policy interventions to control inflation by the central bank will not be effective when the cause comes from the increase in commodity prices. We observe that many global central banks have signalled to accept the scenario of increasing inflation during the recovery period and not being too rigid with the medium-term inflation target.

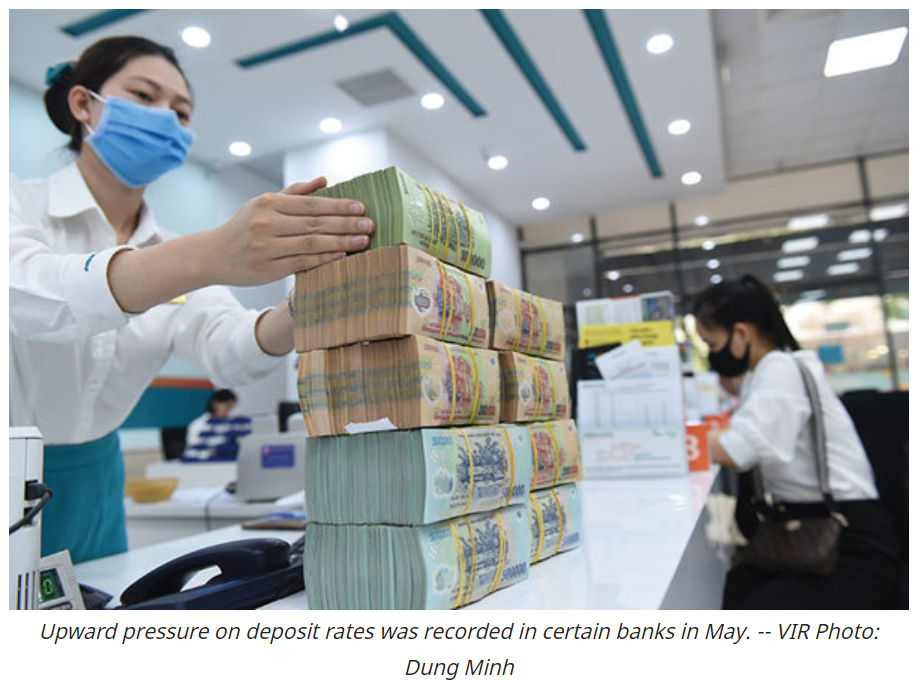

In May, upward pressure on deposit rates was recorded in certain banks. However, we believe that upward pressure may not dominate the whole system, and these actions of certain banks in order to balance the interests of depositors can reduce the trend of diversification into other investment channels. In addition, it is expected to rebalance deposit growth while credit growth has increased faster in the first months of the year.

On the other hand, the direction is maintaining low lending rates to support businesses, and there is still room for further reduction when lending rates have not had a corresponding reduction in deposit rates.

In the last months of the year, we forecast that deposit rates may move sideways or increase slightly by 10-20 points while lending rates will have room to decrease further, but the reduction will not spread across the system.

The SBV has resources to stabilise the exchange rate as foreign reserves are gradually built up over the years along with the effectiveness of foreign currency forward contracts in 2021. The cautious intervention is a necessary factor and special priority when considering the risk that the US may return Vietnam to the list of currency manipulators as happened in 2020, although it was removed in April this year.

In 2020, Vietnam made a record trade surplus of $19.94 billion. However, this trend comes from a decrease in the import of production materials. In 2021, when this trend reverses, especially in the context of high prices of goods and raw materials, the trade balance will be a deficit in 2021. There is a high probability that the SBV may sell foreign currency to intervene in the market.

We predict some possible risks and perils for Vietnam in the coming time. In a broader context, the world economy grew slowly and unsustainably leading to the global economic crisis. Meanwhile, Vietnam suddenly encountered difficulties in pandemic control. Commodity prices continued to increase rapidly and abnormally. There has been no sign of adjustment, leading to difficulties in the supply of production materials. In general, these are assumptions for the worst-case scenario and we do not appreciate the possibility of this scenario.

Source: VIR