Thailand

Thailand

Thailand: Retail market demonstrating solid signs of improvement

Driven by economic growth and a rebound in tourism, the retail property market has been steadily improving since the fourth quarter of last year, with a prediction that it will return to normal by 2024, according to consultants.

Carlos Martinez, director of research and consultancy at Knight Frank Thailand, said the retail market shows signs of recovery, with the tourism sector playing a crucial role.

“As tourists are big spenders, the growth in categories such as food and beverage, shopping and entertainment is anticipated to continue post-pandemic, with hypermarkets expected to benefit from this trend,” he said.

The retail sector has gradually recovered with occupancy rates and average rents for hypermarket retail venues and shopping malls expected to return to the normal rates recorded before Covid-19 by 2024, Mr Martinez said.

The hypermarket sector is focused on expanding in urban areas with a population of over 300,000 residents.

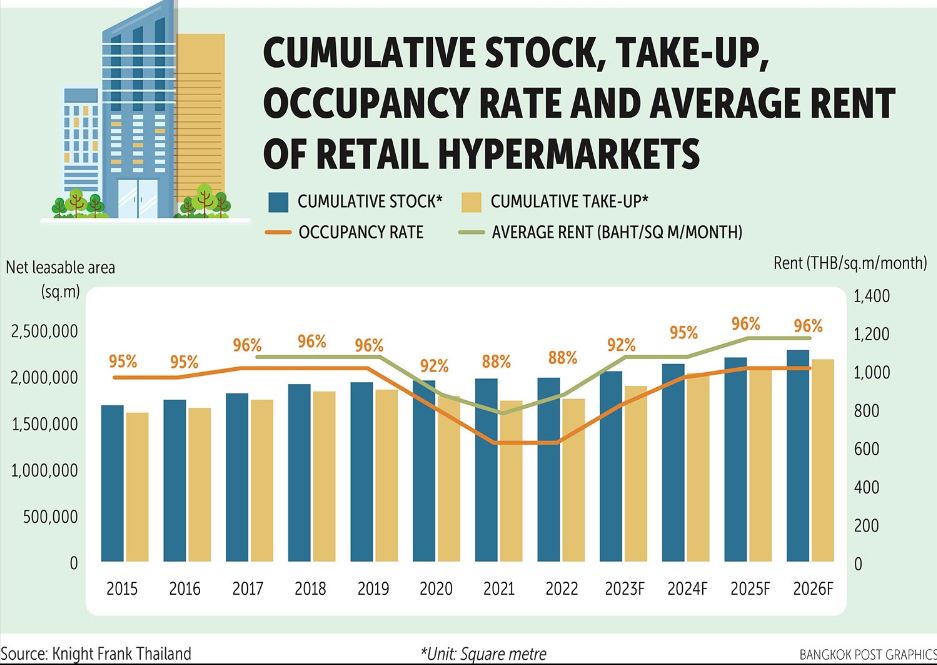

The number of hypermarkets in urban areas increased from 181 out of 266 in 2012 to 254 out of 377 in 2022.

Retail space in hypermarkets leased out to other tenants had high occupancy rates at 95-96% between 2015 and 2019 before declining to 88% in 2021-22.

Despite these challenges, the hypermarket sector demonstrated resilience and endured a relatively low decline in occupancy rates compared to other industries because they could open during lockdowns.

The average monthly rental rate of retail in hypermarkets remained stable at under 1,100 baht per square metre per month from 2017 to 2019, but dropped to its lowest at 755 baht in 2021.

Last year it recovered to 870 baht and will return to the rate seen before the pandemic in late 2023, followed by annual growth rates of 3% and 2% in 2024 and 2025, respectively.

Typically, hypermarkets have a lower average rental rate, often more than 30% lower than shopping malls due to their secondary location, target customer base and reduced operating costs.

“Both hypermarkets and shopping malls saw a decline in occupancy and rents during the pandemic,” he said. “Since the country fully reopened in the second half of 2022, there has been a recovery in both sectors.”

Shopping malls saw a more significant rebound as rents for retail space increased 41% year-on-year in 2022 compared to a 15% increase of hypermarket.

This discrepancy was largely due to the end of rent waivers offered by retail operators to tenants, which had a more pronounced effect on shopping malls than hypermarkets, as a measure to maintain high occupancy levels during the pandemic.

Despite facing competition from e-commerce retailers and smaller specialised stores, hypermarkets have proven to be resilient due to their competitive pricing and extensive product range, as well as their larger physical presence.

To remain competitive, hypermarkets strategically repositioned as destination venues by dedicating a larger portion of space to amenities such as restaurants, cafes and play areas, which led to an enhanced shopping experience for customers.

Hypermarket operators also made significant investments in their own e-commerce platforms, and successfully utilised their established physical infrastructure to facilitate online operations.

Jariya Thumtrongkitkul, head of retail at CBRE Thailand, said the retail market had been steadily improving since the end of last year.

The market started to become more active than it was during the pandemic.

“In Bangkok’s central business district, there are many plans for large retail projects with six projects under construction and seven more for which developers announced their investment plans,” she said.

As a result, there will be an increase in net leasable area in Bangkok of more than a million sq m. The challenge is to create unique, interesting projects and most importantly to meet demand, she said.

Ms Jariya suggested a variety of shops with a balanced, diverse merchandise mix and appealing anchors that can act as magnets to draw shopper traffic and to achieve full occupancy in their leasable spaces.

Source: https://www.bangkokpost.com/business/2558861/retail-market-demonstrating-solid-signs-of-improvement