Thailand

Thailand

Philippines tries to go long to arrest shortening debt maturities

MANILA, Philippines — The Philippines is out to test investors’ appetite for longer-dated debts in a bid to stop maturities from further deteriorating and put limited government resources in a bind, no thanks to last year’s borrowing spree.

Fiscal planners and observers are however not worried that more obligations are falling due much earlier than 2 years ago, counting on the government’s ability to borrow at cheaper costs as well as trillions in liquidity still searching for a viable investment outlet to grow during hard times.

The plan is off to a good start: P35 billion worth of 20-year Treasury bonds were sold for the first time in over a year on Tuesday. Bids were also nearly twice the offer, suggesting that investors are becoming more comfortable locking in their cash for as long as inflation worries begin to subside.

“Auction signals investors are open to long-term tenors with good yield pick-up and shield from inflation,” National Treasurer Rosalia de Leon said in a Viber message.

Whether or not the Treasury would pick up on that signal and sell more longer-dated papers from here on remains to be seen. But it is crucial they do so fast. Last year’s borrowing binge accumulated billions of pesos in debts payable between 3 months and 3 years, a payment period so short, it risks diverting budget funds from public programs to interest settlements.

On one hand, the government was left with no choice but to raise cash as fast as it can to finance a costly pandemic response. There was an option to do so by borrowing long, but that risked attracting fewer demand and in turn, paying higher interest rates.

“We also do not want that since we need the resources to pay for our bills in the pandemic,” a Treasury source said in a phone interview.

The result was a drastic shortening of payment terms. As of end-2020, existing debts are payable by 7.57 years on average, the shortest in 15 years. Broken down, the situation is worse for peso-denominated obligations which, on average, are falling due within 5.45 years— which theoretically means the next administration would spend most of its 6-year term paying debts and their interest.

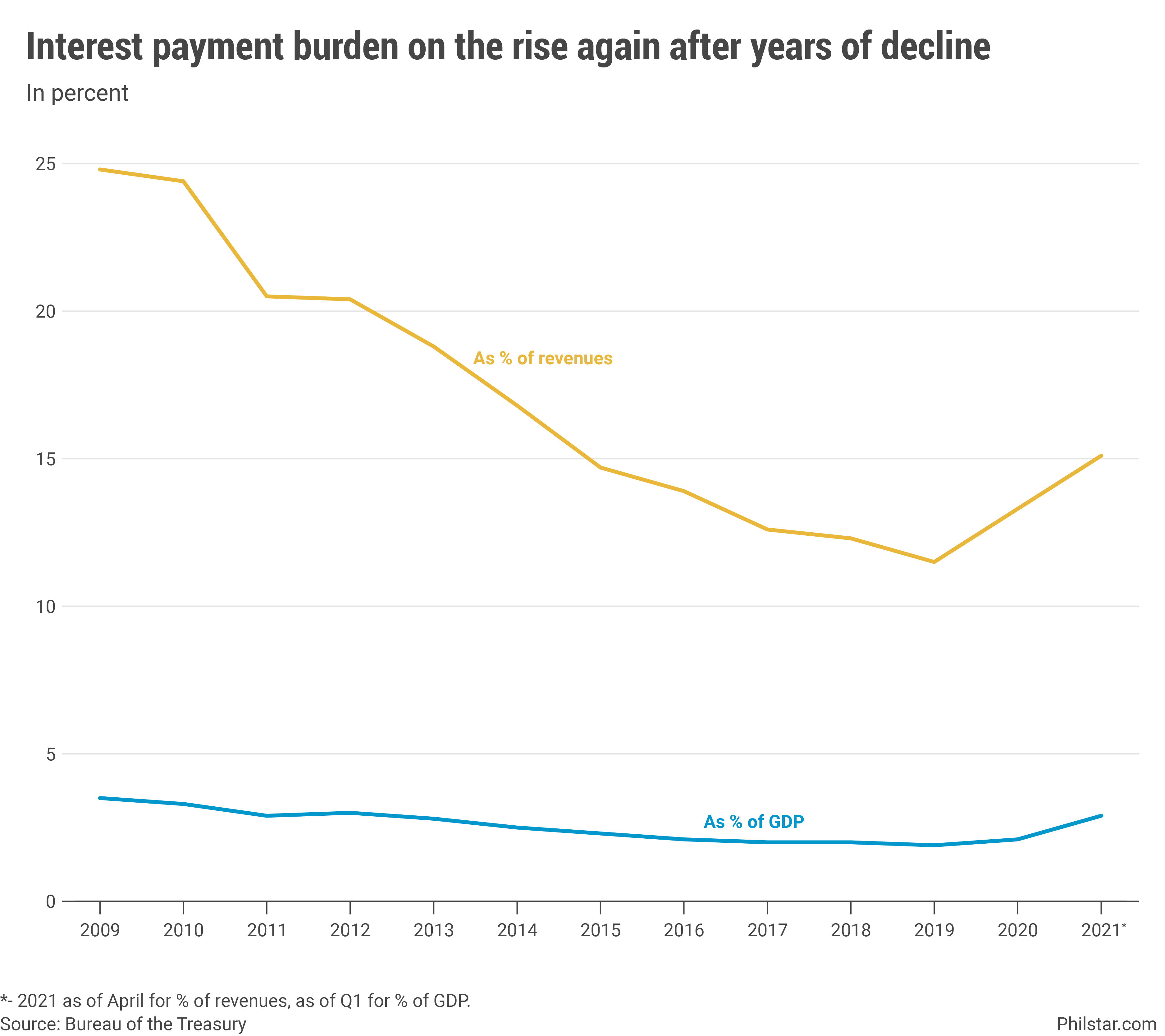

On the flip side, government benefited from the lower interest regime. Debts fetched a weighted average of 4.17% in interest last year, the lowest in available record from 2008. But with larger debts to service, any savings from interest payments are easily blunted— interest payments were already equivalent to 15.1% of revenues as of April, up from 13.3% last year which was already a 4-year high.

But for analysts, the Philippines had been in worse shape during past crises, suffering a combo of shorter maturities and high interest in the 1997 and 2008 financial meltdowns. At the time, over 36% of revenues went to just meeting interest payments, depriving the economy of investment funding. Things have drastically turned around since then.

“As for comparing past crises with the current crisis, we can say that the Philippines is definitely in better fiscal shape and its profile more robust owing to better credit ratings and a likely bias for domestic debt in 2020 as opposed to previous episodes which also helps mitigate currency risk,” Nicholas Mapa, senior economist at ING Bank in Manila, said.

“Meanwhile, authorities have also been vigilant in issuing debt that is not as susceptible to interest rate fluctuations, thus also insulating the Philippines from interest rate risk,” Mapa added.

In fact, for Antonio Agcaoili, executive vice-president and treasurer at Asia United Bank Corp., that shorter-dated debts are now preferred may be considered a demonstration of that fiscal strength.

“Perhaps it can also be argued that the deliberate effort to shorten their maturity profile is indicative of the Finance Officials’ (both BSP and BTr) level of confidence in their ability to manage the overall level of inflation, as well as fiscal and budget deficits,” he said in an email

Jose Emmanuel Hilado, chief financial officer and treasurer at UnionBank of the Philippines, believes there would still be time to improve the country’s debt profile by next year, when inoculations and stable inflation would likely keep credit costs low.

“I think the market for longer maturities will slowly come back this year. The investors will just have to contend with what happens to the global markets especially in the U.S. where bond yields have been going up due to inflation fears,” Hilado said.

Source: https://www.philstar.com/business/2021/06/01/2102605/philippines-tries-go-long-arrest-shortening-debt-maturities