Thailand

Thailand

Philippines: Not all deficits are created equal

MANILA, Philippines — A celebrated playwright and coincidentally one of the founders of London School of Economics and Political Science (LSE), George Bernard Shaw once famously quipped “If all economists were laid end to end, they would not reach a conclusion.”

Economics as a field has been characterized by a number of disagreements. One only has to look at the epic debate between Friedrich Hayek and John Maynard Keynes to realize this. Even expressions associated with the field such as “two sides of the same coin” and “there are many ways to skin a cat” connote a certain sense of ambivalence. Indeed, economists often “agree to disagree.”

Speaking of disagreements, one concept that has been a frequent subject of passionate debate among economists is the implications of current account (CA) imbalances. This is a very timely issue for the Philippines as the country’s CA balance reversed to a deficit, after 13 years of consecutive surpluses.

Naturally, this triggered concerns among policymakers and economists alike. But what does this really mean and should we really be worried?

Too many ways to skin a cat

Just as there are many ways to skin a cat, the concept of current account can also be interpreted in several ways.

First, the simplest interpretation of CA is the difference between a country’s value of exports and the value of its imports. A deficit then means that a country is importing more goods than it is exporting. This naturally points to issues of competitiveness. Are the country’s exports less competitive than other countries’ exports? The concept of competitiveness is very elusive and multi-faceted and deserves a more extensive discussion in another article.

But if the deficit is not an issue of competitiveness, is it therefore just a simple case of a country importing more because its economy is growing? Are we forgetting that the main reason to export is to be able to import what we need?

Another interpretation of the CA is the difference between the country’s savings and investment. A current account deficit, therefore, could mean that a country has low national savings relative to investment or it could equally mean that an economy is highly productive and is robustly growing with many opportunities for productive investments.

Clearly, there is no straightforward answer. We need to know the underlying causes of such a deficit to allow for an appropriate assessment of whether a deficit is favorable or unfavorable for an economy at any given time.

CA dynamics in the Philippines

In the Philippines, the CA balance swung to almost a $1 billion deficit in the 2016 revised balance of payments (BOP) data. This was a reversal from the $7.3 billion surplus in 2015.

This resulted primarily from the widening of the trade-in-goods deficit as imports growth significantly outpaced exports growth.

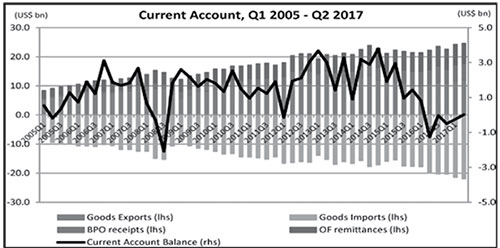

One should recall that the country’s trade-in-goods position has always been in deficit even when the CA has been recording surpluses annually since 2003. However, in the past two years, the trade-in-goods deficit widened by 34.5 percent in 2015 and 52.5 percent in 2016, making it large enough to cause a significant decline in the CA balance. This followed from the combined effects of goods exports declining sharply (Q3 2014 and Q3 2015) – on account of weak global demand compounded by falling commodity prices – and imports increasing markedly (Chart 1) on account of robust output growth.

There has been quite a strong demand for imports since Q1 2016 (minimal growth recorded in Q4 2015 after three quarters of contraction). Double-digit increases were particularly noted for capital goods, raw materials and intermediate goods, a trend which is actually positive for the economy.

Chart 1.

Notes: BPM6 Concept

Source: BSP

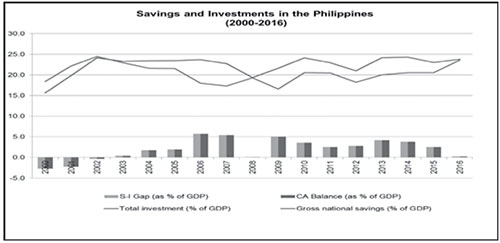

Chart 2.

Source: IMF WEO Database and BSP

In terms of savings and investment, for the Philippines, the savings-investment gap has stayed positive since 2003 (hence the CA surpluses since this period) but has started to converge in 2015 due mainly to the rise in investments and increase in infrastructure spending (Chart 2).

There is no such thing as a free lunch

So what are the underlying trends driving the recent CA deficit of the Philippine economy?

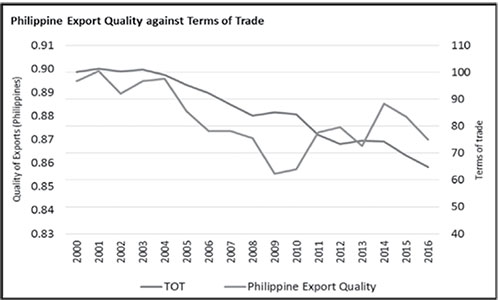

In terms of the difference between exports and imports, the premise is that the Philippine economy is growing. Thus, one should expect that this will be accompanied by stronger demand for imports, reflecting the sustained rise in business and production activities to support economic growth. Since economic growth entails rising incomes, and consequently stronger demand for goods, including those for imported capital used for business expansion, the country’s terms-of-trade (the ratio between a country’s price of exports to its imports’ prices) has been declining (Chart 3).

Moreover, data appears to suggest that the current rise in imports relative to exports is not indicative of competitiveness issues. In fact, despite the decline in the terms of trade (TOT), the quality of Philippine exports has recovered from its levels before the crisis.

Chart 3.

Source: IMF, PSA, and BSP Staff Calculations

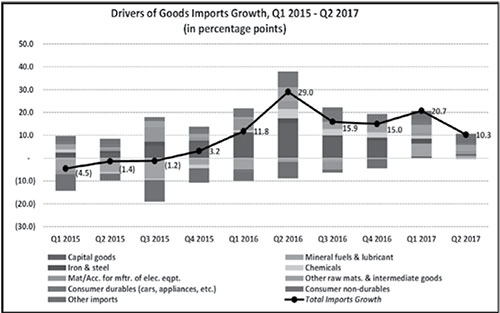

Likewise, our import-mix reflects not only the sustained but also broad-based expansion in the domestic economy’s capital formation, production, and consumption. Imports of goods in the first half of 2017 amounted to $43.4 billion, posting a 15.2 percent increment relative to $37.7 billion in the same period last year. The year-on-year expansion was boosted primarily by increased imports of raw materials and intermediate goods (by 16.8 percent), mainly supported by materials and accessories used for manufacture of non-consigned electronics. Imports of mineral fuels and lubricants grew by 30.7 percent, buoyed by the hike in global oil prices which averaged about $51.32 per barrel in the first half of 2017, from an average of $36.75 per barrel in the comparable period in 2016. These economic activities, in turn, should help expand the economy’s potential capacity and support the needed infrastructure development (Chart 4) in the succeeding years.

This development is consistent with empirical studies as well as the results of the BSP’s own assessment which shows that the Philippine CA is driven primarily by domestic demand and terms of trade shocks.

Chart 4.

Notes: BPM6

Source: PSA and BSP

The narrative of the country’s growth is also consistent when the deficit is viewed in terms of the savings-investment gap. High growth leads to residents investing abroad and prepaying their external debt. In the first quarter of 2017, residents’ direct investments and business activities abroad grew by 45.1 percent compared to last year. Moreover, resident’s debt prepayments also rose by 54.3 percent (y-o-y) in the first semester of 2017. Portfolio investments by residents also increased by 15.5 percent (y-o-y) in the first quarter of 2017.

All these trends appear to suggest that the Philippine economy’s CA and balance of payments deficits are indeed driven by the country’s solid growth dynamics. In particular, the increase in imports point to the continued expansion in the domestic economy’s capital formation and production – one has to spend in order to make money so to speak.

This broad-based growth in imports reflects the sustained rise in business and production activities in the economy. Hence, the peso’s depreciation can be viewed as necessary to support the country’s expansion. Our data shows that imports accelerated in the last two years, indicating some frontloading of imported durable goods. Such may now be moderating and helping reduce the depreciation pressures on the peso. On top of that, we have also seen exports recovering starting in 2017 in a big way so that the outlook on the trade-in-goods is more promising.

As history would attest, the peso’s value has always moved along with the “demand for” (by those who need foreign currency) and “supply of” (by those who have foreign currencies) foreign exchange in the economy.

Not all deficits are created equal

Running a current account deficit may not necessarily be a cause of concern depending on the underlying economic trends. It all depends on how the deficit came about and how it is to be financed.

In the case of the Philippines, the deficits are mostly driven by increasing import demands that are consistent with robust domestic economic activity. In addition, the National Government’s commitment to boost infrastructure spending suggests that these deficits would be used to finance productive investments.

Lastly, other factors offer support to this narrative of growth such as the large overseas Filipino remittances, robust receipts from both business process outsourcing and tourism, and strong inflows of foreign direct investments (FDI). At the same time, there is a steady decline in Philippine external debt as a percent of GDP while the level of gross international reserves remains ample.

Context is, therefore, critical in understanding economic developments including the emerging current account shortfall.

The truth of the matter is, not all deficits are created equal.

Source: http://www.philstar.com/business/2017/11/03/1754970/not-all-deficits-are-created-equal