Thailand

Thailand

Most Singapore households able to continue servicing mortgages amid rising interest rates

MOST Singapore households are able to continue servicing mortgages for their homes in the face of rising interest rates, ministers told Parliament on Thursday (Oct 10).

Alvin Tan, Minister of State for Trade and Industry, said household debt as a whole remained healthy, and stress tests conducted by the Monetary Authority of Singapore (MAS) suggest that most households are able to service their home loans, while “a relatively small portion may be more constrained”.

He said these stress tests examined debt-repayment ability based on income; financial buffers such as savings were excluded. Scenarios tested included further interest rate hikes and significant income losses, “even under a 400 basis point increase and a 10 per cent reduction in income”.

Tan was responding to questions on the proportion of homeowners with loans from private financial institutions who had been affected by the rise in interest rates, and the risk and magnitude of foreclosures in the near- to medium-term.

As of the second quarter of 2022, one in three homeowners with outstanding mortgages from financial institutions (FIs) are on mortgage packages that move with market interest rates. “These borrowers have already seen mortgage repayments rise over the past months,” said Tan. The remaining borrowers’ loans are fixed, or fixed for a period, or tracking market rates with some lag.

Tan said: “The proportion of non-performing mortgages among FI loans is low, at 0.3 per cent. The number of foreclosures has in fact trended down since 2021, and remained low at fewer than 30 units so far this year. MAS does not expect widespread foreclosures in the near to medium term.”

In a separate written reply, Minister-in-charge of MAS Tharman Shanmugaratnam said that as of Q2 2022, about 37 per cent of FI loans for private residential property specifically were on floating rate packages.

Among public housing flat-owners, about 80 per cent with loans from FIs are on mortgage packages that track market interest rates, but with some lag. The remaining 20 per cent, who are on packages that move with market interest rates, have seen their repayments rise over the past months, said Desmond Lee, Minister for National Development.

Borrowers on housing loans from the Housing Development Board have not been affected by rising rates, as the HDB concessionary loan rate is unchanged at 2.60 per cent, he noted. Non-performing mortgages among HDB flat owners has remained low and stable for housing loans extended by both HDB and FIs.

Lee was replying to questions on the impact of higher interest rates on those who have taken out housing loans to finance their HDB and private home purchases. He added that government agencies had various financial assistance measures in place to help homeowners in distress.

The government recently announced measures to tighten housing loan limits amid rising interest rates, raising the medium-term interest rate floor used to compute the Total Debt Servicing Ratio (TDSR) and MSR for property loans by FIs. Housing loans granted by HDB are now subject to an interest rate floor to compute eligible loan amounts.

The recent round of cooling measures for the property market, which took effect on Sep 20, also imposed a 15-month waiting period for existing and former private residential property owners wanting to buy HDB resale flats.

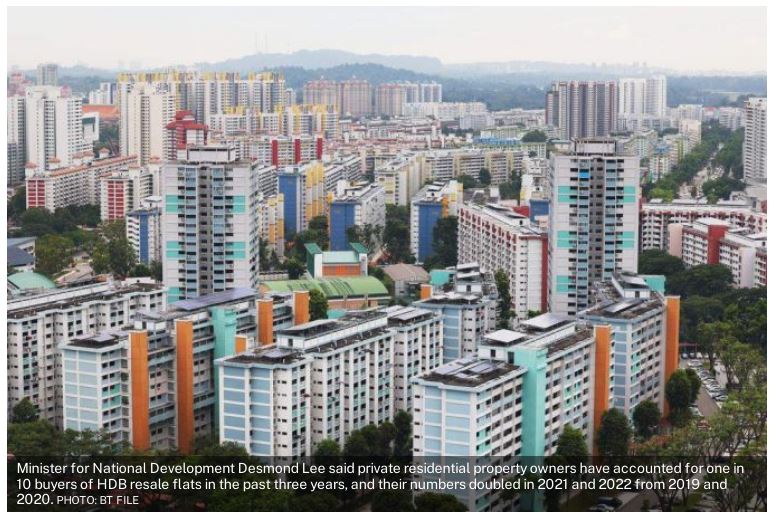

Private residential property owners have accounted for one in 10 buyers of HDB resale flats in the past three years, and the numbers doubled in 2021 and 2022 from 2019 and 2020, Lee noted on Thursday. On the matter of cash-over-valuation (COV), more existing and former private residential property owners than other buyers of HDB resale flats pay this – and pay higher COV amounts as well.

The aim of introducing the wait-out period “is to monitor demand for properties from private property owners cashing out and going to the HDB resale market, in order to give priority to first-time homebuyers”, Lee said, in replying to questions on the impact of the recent cooling measures.

He noted that the 15-month wait-out period is not the first-of-its-kind measure to be implemented: For instance, to receive CPF housing grants when purchasing HDB resale flats, buyers must not have disposed of any private properties in the last 30 months. This rule has been in place since 1975.

Since the implementation of the 15-month wait-out, HDB has received some 650 appeals, Lee said. This includes appeals from 220 homeseekers who had obtained an option to purchase (OTP) for an HDB resale flat before the wait-out period was implemented. HDB has waived the 15-month wait-out period for these 220 flat buyers.

The rest of the appeals – which HDB will assess on a case-by-case basis – came from homeseekers who had yet to obtain an OTP, but had already committed to sell or have sold their existing private property, said Lee.

Describing the public housing market as “buoyant” since the first quarter of 2020, Lee noted that the HDB Resale Price Index (RPI) declined by 9.9 per cent between 2014-2018 and remained flat in 2019. “The increase in resale HDB flat prices during the last two years of the pandemic reflects broad-based demand for housing, supported by the previous low interest rate environment,” the minister added.

“We will consider the prevailing economic and market conditions, including the impact of the 15-month wait-out period, as we plan our half-yearly government land sales (GLS) supply for private housing.”

The government has already moved to enlarge the supply of private housing from its Confirmed List of the GLS programme by 75 per cent, from around 3,600 units in 2021 to around 6,300 units in 2022. “We are prepared to increase the GLS supply further, if needed,” Lee said.

Source: https://www.businesstimes.com.sg/real-estate/most-singapore-households-able-to-continue-servicing-mortgages-amid-rising-interest