Thailand

Thailand

Thailand sidesteps currency storm

The domestic economy looks safe and sound amid a wave of emerging-market turmoil, in stark contrast with 1997, when Thailand gave rise to an economic contagion that spread across Asia.

The country’s large current account surplus and foreign reserves, plus a low level of public and foreign-denominated debt, should cushion any impact from the Indonesian rupiah’s slide, said Sorapol Tulayasatien, director of the Fiscal Policy Office’s Bureau of Macroeconomic Policy.

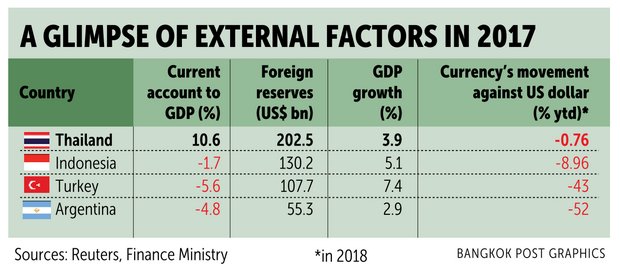

Thailand’s current account surplus totalled US$21.4 billion (701.8 billion baht) at the end of June, compared with a $49.3-billion surplus for the full year of 2017. Public debt was relatively low at 40.9% of GDP at the end of July. Foreign currency debt accounted for 4.17% of public debt at the end of May.

Foreign reserves were almost $205 billion as of Aug 24, or 3.5 times short-term debt.

Mr Sorapol’s remarks came after the rupiah slumped to 14,933 against the US dollar, a two-decade low, on Wednesday amid capital flight as investors feared currency contagion from emerging markets like Argentina and Turkey.

Mr Sorapol’s remarks came after the rupiah slumped to 14,933 against the US dollar, a two-decade low, on Wednesday amid capital flight as investors feared currency contagion from emerging markets like Argentina and Turkey.

The rupiah slump sent emerging stock markets lower on Wednesday, with the Thai bourse down 1.6%.

Mr Sorapol said the US-China trade dispute and Turkish economic woes have whittled investor appetite for risk assets and compelled them to readjust their portfolios by lowering asset allocation in emerging markets, particularly perceived as high-risk.

In Thailand, foreign investors have shunned stocks and shifted to bonds, he said.

But the impact from the foreign sell-off on Thai equities is far less than in other emerging markets: the SET index is down 3% year-to-date, while Indonesian and Chinese stocks have plunged 20% and 18% respectively, Mr Sorapol said.

Bank of Thailand governor Veerathai Santiprabhob last week voiced concerns about offshore funds flowing into Thailand at a faster pace relative to regional peers, pouring mostly into short-dated bonds. The baht has strengthened about 1.7% versus the greenback since Aug 15, though it weakened 0.7% from Aug 27.

Roong Sanguanruang, head of global market research and analysis, at Bank of Ayudhya, said the baht is showing a bias for further weakness to 33 against the dollar this week, tracking the rupiah’s skid.

Even so, the baht has outperformed other regional currencies since the start of the week, down 0.3%, outdoing the Singaporean dollar (-0.4%), the Malaysian ringgit (-0.5%) and the Philippine peso and Indonesian rupiah (-0.6% each).

Impact from the rupiah tumble’s on the baht will be limited and won’t snowball into a regional currency crisis, Ms Roong said, unlike Turkey’s and Venezuela’s cases.

She said Thailand’s sound economic fundamentals, including a high current account surplus, strong international reserves and low foreign debt, will serve as a buffer.

But the baht’s swings may continue because of several uncertainties in the global market, including trade rows, currency crises in emerging markets and US interest rate hikes, Ms Roong said, adding that such negative factors will affect foreign capital flows and currencies worldwide.

Source: https://www.bangkokpost.com/business/finance/1535514/thailand-sidesteps-currency-storm