English

English

Singapore’s exports to remain weak as March data marks half year of contraction: economists

SINGAPORE’S key exports are expected to record further weakness in the months ahead, after declining for the sixth consecutive month in March, on the back of challenging global economic conditions, economists said.

“Global demand will likely stay weak amid tight monetary policy in advanced economies and vulnerabilities in the financial system following the banking turmoil in US and Europe,” said Maybank economists Chua Hak Bin and Lee Ju Ye.

Non-oil domestic exports (NODX) fell 8.3 per cent year on year, moderating from February’s 15.8 per cent year-on-year decline, Enterprise Singapore data showed on Monday (Apr 17). It was better than the median 19.4 per cent fall forecast by economists in a Bloomberg poll.

On a seasonally-adjusted monthly basis, NODX jumped 18.4 per cent last month, reversing February’s 8.2 per cent decrease.

Still, economists remained downbeat on Singapore’s export performance in the coming months. UOB senior economist Alvin Liew anticipates “a few more months” of year-on-year declines in H1, before some improvement in the later half of the year.

Barclays senior regional economist Brian Tan said that while March’s sequential surge surprised on the upside, details suggest that it was partly a normalisation of shipments following the weak February numbers, with a little help from the usually volatile segments such as pharmaceuticals, non-monetary gold and oil rigs.

Electronics exports, though posting a sequential rise, were back only to January levels, he added.

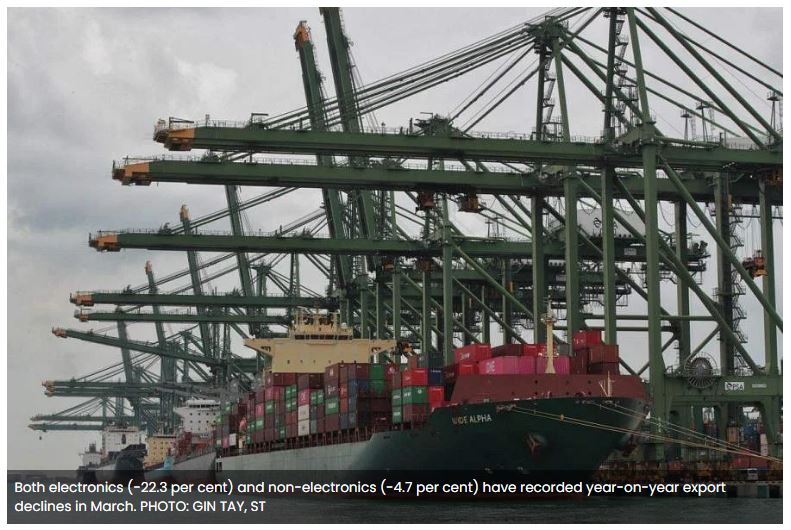

On the year, both electronics (-22.3 per cent) and non-electronics (-4.7 per cent) shipments declined.

Citing the Monetary Authority of Singapore’s (MAS) latest Monetary Policy Statement, Liew said that the global electronics industry is in a sharp downturn, and that the “drag on global investment and manufacturing from tighter financial conditions will intensify in the quarters ahead”.

On non-electronics, the Maybank team noted that exports shrank at the softest pace in six months, but this was cushioned by pharmaceuticals, where there is low correlation between production and exports. The industry’s volatility, OCBC chief economist Selena Ling said, suggests that it is too early to call an end to the NODX soft patch.

Economists also highlighted the limited impact of China’s reopening. In March, NODX to eight of Singapore’s 10 top markets reported year-on-year declines, with exceptions being the US (13.2 per cent) and South Korea (3.1 per cent).

Falls in shipments to China (-14.1 per cent) was the largest dampener to growth, said the Maybank team. “China’s reopening has so far largely driven a rebound in consumption and domestic services.”

Maybank’s team continued: “China’s demand for intermediate products remain weak, as implied by the worsening exports to China from South Korea, Taiwan and Vietnam. China’s reopening and recovery may drive stronger import demand in the second half of the year.”

OCBC’s Ling said that China’s export recovery, led by shipments to Asean, reversed five consecutive months of weakness. But she also noted that “anecdotal Chinese evidence are less stellar as shipping freight rates have dipped and the container availability index remains elevated”.

She added that this may explain Premier Li Qiang’s recent comments that there is a need to help exporters secure orders and expand markets with a combination of trade stabilisation policies, and try to stabilise exports to developed economies and guide exporters to explore the markets of developing countries and Asean.

Liew noted that MAS also projected a growth slowdown in Singapore’s major trading partners in 2023, compared to the two preceding years.

UOB maintained its full-year NODX forecast at a contraction of -5.5 per cent. Maybank kept its forecast at between -7 per cent and -4 per cent, while OCBC maintained its prediction at around -3 per cent.

After the NODX figures were released, both Maybank and OCBC maintained their gross domestic product (GDP) growth forecasts at 0.8 per cent and 1.5 per cent respectively, which they had previously cut following the “disappointing” Q1 2023 GDP growth performance.

Chua and Lee added: “We expect the MAS to maintain the current appreciation stance at the October meeting, as core inflation decelerates in the second half of the year while growth stagnates.”

Barclays’ Tan also said that monetary policy is unlikely to further tighten – with recent inflation prints matching expectations – while the bar for easing is high, given still-elevated prices and a goods and services tax hike on the horizon.

However, “should the MAS believe the output gap is about to turn significantly positive again”, he does not rule out a 50 basis point increase.

Source: https://www.businesstimes.com.sg/singapore/singapores-exports-remain-weak-march-data-marks-half-year-contraction-economists