English

English

Singapore: Secure ecosystem is key in fast payment access for non-bank e-wallet players

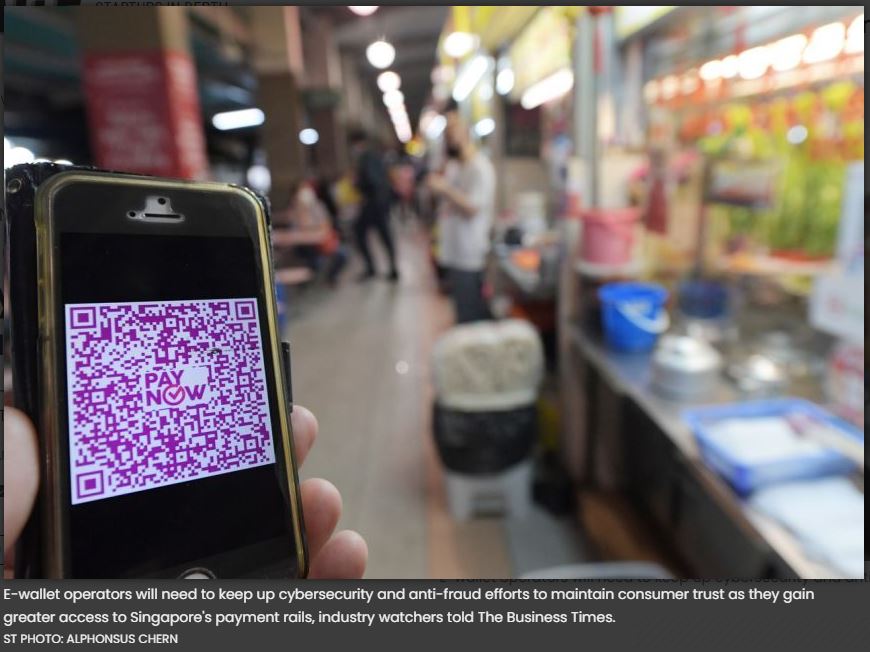

E-WALLET operators will need to keep up cybersecurity and anti-fraud efforts to maintain consumer trust as they gain greater access to Singapore’s payment rails, industry watchers told The Business Times.

On Monday, the Monetary Authority of Singapore (MAS) announced that eligible non-bank financial institutions (NFIs) will have direct access to the banking system’s real-time retail payments infrastructure, FAST and PayNow, from February 2021.

This means that consumers would be able to top up non-bank e-wallets from their bank accounts, as well as move funds across e-wallets. At present, most e-wallets require a debit or credit cards to top up funds, and transfers between e-wallets are not possible.

FAST allows customers of participating entities to transfer Singapore dollar funds from one entity to another instantly. PayNow, which runs atop FAST, allows transfers to be made using a convenient proxy, such as a mobile number, NRIC number, or a business’ Unique Entity Number.

E-wallet operators and industry experts BT spoke to cheered MAS’ move as a milestone, citing that the cost savings will level the playing field and promote fintech innovation.

But the experts also emphasised that building a secure and credible digital payments ecosystem is vital, given a recent spate of cybersecurity incidents.

“Consumers will have to trust the use of FAST and PayNow by NFIs’ apps. Many users are still worried about storing their credit card details in apps and websites. Here, we are asking them to connect their bank accounts for direct debits,” noted Jan Ondrus, an associate professor of information systems at ESSEC Business School Asia-Pacific.

Singapore has put in place strict requirements for cybersecurity as a “non-negotiable” aspect for fintechs, said Varun Mittal, EY global emerging markets fintech leader. To maintain trust, he reckons that players can invest further in risk management.

“If somebody is not a user of a service, but suddenly there is a S$500 charge, then how do you protect (against) that? How to proactively stop it? This is why fraud, risk management, early warning systems are very important,” he noted.

For their part, e-wallet operators told BT that they are investing more resources into these areas. Eduard Fabian, chief technology officer at Razer Fintech, said: “We are very watchful. We have increased our investments into people, processes and technology, in the cybersecurity part, but also in terms of fraud management and anti-money laundering.”

Likewise, Jeremy Tan, chief executive of payment services firm Liquid Group, said that it is important for all industry players to not only have secure technology, but to also step up customer education on phishing.

Razer Fintech and Liquid Group are part of the Direct FAST Working Group that worked with the MAS on this effort. Fellow members include Grab Financial Group, MatchMove, Singtel Dash and TransferWise.

MAS’ move is widely seen as a win for fintechs against the financial incumbents, from a cost perspective.

“Typical e-payment processing costs are between one per cent to 2 per cent. With PayNow, we expect a savings of at least one per cent per transaction. However, on a blended cost basis, overall payment costs remain to be seen,” said Ng Aik Phong, managing director of Fave Singapore and Malaysia.

Meanwhile, “it seems that the big losers are the card schemes such as Visa, Mastercard, and Amex. The new setup would bypass their network. Therefore, there will be some financial losses on their side”, said Assoc Prof Ondrus.

Conversely, fintechs addressing cross-border payments could especially benefit, as “this will simplify and hopefully lower the cost for low-value remittances”, said Shirish Jain, director specialised in payments at Strategy&, the consulting arm of PwC.

However, there are also some potential downsides for fintechs. For one, the ability to transfer funds between e-wallets may diminish customer stickiness.

“The wallet providers, who often set up these wallet services and are willing to incur the top-up costs, just to gain access to customer spend and transaction data, may not necessarily end up reaping those data access benefit as before. So, wallet providers… will need to compete more to gain customer traction,” said Umair Hameed, partner for financial services advisory at KPMG.

These operators may also have to bear extra costs to meet the requirements for direct FAST and PayNow access, noted Mr Jain.

In any case, Singapore’s major players are optimistic about MAS’ move, saying that it paves the way for more innovative products.

Lim Kell Jay, head of Grab Financial Group Singapore, said that “the integration gives us greater flexibility in designing more consumer-centric financial solutions such as new micro-investment products”.

Beyond instant top-ups, users of Singtel Dash would also be able to make payments at over 200,000 businesses that accept PayNow, noted Arthur Lang, CEO of Singtel’s International Group. “This partnership… demonstrates our commitment to grow Dash into an all-in-one app to meet the needs of digitally savvy consumers,” he said.

As Mr Fabian of Razer Fintech puts it: “We cannot foresee all the innovation that is going to come by opening up the ecosystem and levelling the playing field, but that’s the most exciting part.”

Source: https://www.businesstimes.com.sg/garage/sff-x-switch-2020/secure-ecosystem-is-key-in-fast-payment-access-for-non-bank-e-wallet