Thailand

Thailand

Singapore: As manufacturing slows, diverse factors may drive 2019 growth

AS CLOUDS of global uncertainty show no sign of lifting and Singapore’s manufacturing industry – its erstwhile growth driver – continues to cool from a once red-hot pace, it may seem unclear where the country should look to for growth in 2019.

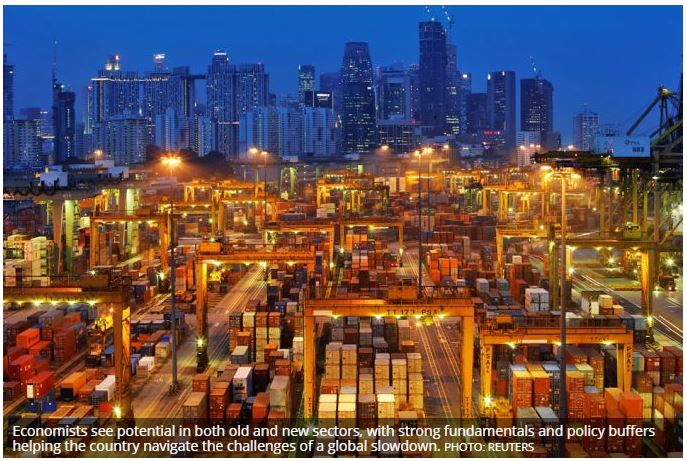

Still, economists see potential in sectors both old and new, with growth staying relatively resilient in the face of weaker external demand and allowing the possibility of further monetary tigtening ahead.

Compared to this year’s 3 to 3.5 per cent range, the official growth estimate for 2019 is 1.5 to 3.5 per cent, with most economists expecting it to come in within 2.5 to 3 per cent.

The Ministry of Trade and Industry’s “downwardly biased” outlook is justified by hard-to-quantify downside risks such as trade frictions and tighter financial conditions, said Mizuho Bank head of economics and strategy Vishnu Varathan, who expects 2019 growth to be around 3 per cent. But he added: “The bigger picture is that the economy is going over a speed bump, not a cliff.”

Bank of America Merrill Lynch economist Mohamed Faiz Nagutha, whose forecast is for 2.8 per cent growth next year, said: “As a small and open economy, Singapore will bear the brunt of any significant global slowdown, but strong domestic fundamentals and policy buffers should help better navigate the challenges.”

He puts the predicted slowdown in context: After two years of above-trend growth, the economy is expected to “slow back to trend” over 2019 and 2020. “2019 is unlikely to be a spectacular year, but is also unlikely to be a year of crisis.”

Tensions between the United States and China continue to be the main external risk, 90-day truce notwithstanding. OCBC head of treasury research and strategy Selena Ling expects a “slow burn” scenario in the coming year “as a grand resolution or deal is unlikely to be forthcoming”.

In November, Singapore’s non-oil domestic exports fell for the first time since March, down 2.6 per cent from a high year-ago base. Notably, NODX to China fell 16 per cent, having seen year-on-year declines in most months this year apart from April.

ANZ head of Asia research Khoon Goh expects a switch from 2018’s relatively export-led growth. In 2019, net exports are “unlikely to add much to growth and may even subtract”, he said, particularly if imports pick up thanks to strong domestic demand.

With widespread monetary tightening as another dampener on global growth sentiments, Ms Ling sees a “slightly weaker” external demand outlook in 2019, with the manufacturing sector to see a more modest expansion as a result. Her forecast for 2019 growth is 2.7 per cent.

Singapore’s manufacturing purchasing manager’s index (PMI), an indicator of activity, has been trending downward this year, with the electronics sector PMI in particular breaking a 27-month growth streak by dipping into contraction in November.

Still, manufacturing is expected to continue contributing to growth – just at a more moderate level. Mr Varathan sees a possible cushion from continued improvement in the maritime and offshore sector, as well as a boost from the volatile pharmaceuticals sector. And even as electronics slows, there may still be reason for optimism.

Other sectors may help pick up some of the slack. Said Bank of America Merrill Lynch economist Mohamed Faiz Nagutha: “We see greater contribution from services and construction offsetting an expected moderation in manufacturing.”

Though construction has been subdued in recent years, en bloc project deals struck from mid-2017 till cooling measures kicked in this July are likely to get underway in 2019, noted ANZ’s Mr Goh. “Regardless of the external environment, that construction activity will happen.” Investment, including residential investment, will thus be a driver of growth.

Some fiscal boost is also expected if the upcoming Merdeka Generation healthcare package for those born in the 1950s – announced in August with details to come in 2019 – results in higher consumer spending by the target age group, he added.

Citi economists Kit Wei Zheng and Ang Kai Wei noted that possible early elections mean that fiscal policy could take an expansionary turn: “If past elections prove a guide, cash transfers, increased medical and housing subsidies will be on the cards for Budget 2019.”

In services, Mizuho’s Mr Varathan sees a fillip from fintech amid resilience in traditional financial, insurance and business services.

CMC Markets market analyst Margaret Yang pinpoints the Internet economy, including e-commerce, ride hailing, and online media and travel services, as an emerging sector. She noted that it currently accounts for just 3.2 per cent of GDP but has seen a compound annual growth rate of 22 per cent over the last three years.

Against this background of moderating yet resilient growth, which remains slightly above potential, there is a “good chance of further tightening” by the Monetary Authority of Singapore (MAS) if core inflation continues creeping up, said UOB senior economist Alvin Liew. “The key downside risk for inflation will be how global crude oil prices perform.”

Most economists agree that there is room for further MAS tightening in 2019, following two cautious moves this year. OCBC’s Ms Ling cites domestic labour market tightness, which may sustain wage growth and underpin core inflationary pressures if businesses pass on the higher wage costs to consumers.

Source: https://www.businesstimes.com.sg/government-economy/as-manufacturing-slows-diverse-factors-may-drive-2019-growth-0