English

English

Non-traditional services emerge as determant for Vietnamese banks’ income

Net interest income is traditionally the main driver of income for banks. However, in recent years banks have tried to reduce their dependence on lending activities. Income from non-traditional services has emerged as another determining factor of total operating income (TOI) growth, according to Vietnam Dragon Securities Company (VDSC).

In a context of tightening credit growth by the State Bank of Vietnam (SBV), the ability to expand service income becomes even more important. Service income is gaining momentum and contributes more to TOI, in most of the banks under the brokerage’s coverage.

Retail banking is a priority for most banks nowadays, stated VDSC. Banks’ service income has been expanding, mainly due to the high growth of transaction and guarantee fees, as well as more contribution from other value-added products such as insurance, cross-sale services, credit card, e-banking and brokerage activities.

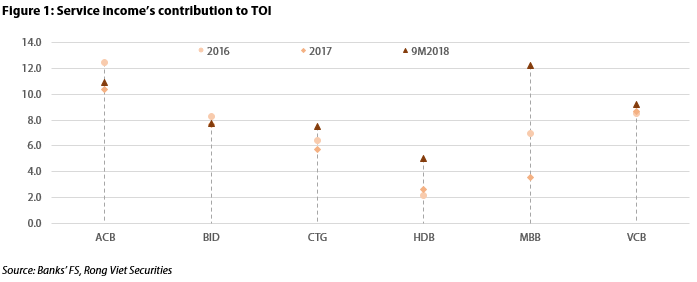

According to VDSC, Asia Commercial Bank (ACB) and Military Bank (MB) have the largest contribution from non-interest income. Ho Chi Minh Development Bank (HDBank) has the lowest but the bank saw the fastest growth momentum in the first nine months of 2018.

In terms of growth momentum, it is followed by MB and Joint Stock Commercial Bank for Foreign Trade of Vietnam (VietinBank). Meanwhile, ACB saw a reduction in service income contribution. The proportion at two state-owned banks, Joint Stock Commercial Bank for Foreign Trade of Vietnam (Vietcombank) and Joint Stock Commercial Bank for Investment and Development of Vietnam (BIDV) is mostly unchanged since 2016.

Service income as growth engine

Though service income of HDBank only contributed to 1.9% of TOI in the first nine months of 2017, the portion has been constantly expanding to 2.6% in 2017 and 5.0% in the first nine months of 2018. This is due to the boost in income from insurance brokerage, which accounts for more than 60% of service income. Considering the very strong growth achieved in the January – September period, VDSC expected that the bank will continue to be a leader in that segment with approximately 150% growth in 2018 and 70% growth in 2019.

MB, in the January – September period, through the increase in the activities of MB Ageas Life, realized a surge in income from insurance, up 220% year-on-year, which in turn drove service income to grow by 62.9% year-on-year. VDSC expected that the bank’s service income growth will reach 80% in 2018 and 50% in 2019, driven by insurance.

Vietinbank also saw a rapid expansion of its service income. It grew 55% year-on-year and accounted for approximately 7.5% of the bank’s TOI in the first nine months of 2018. The bank launched its high-tech core banking platform in February 2017, which is expected to help services income grow by 50% in 2018 and 25 – 30% per annum in the next three years due to higher fees from services, bankcards, insurance, transaction and securities.

In 2018, ACB boosted its service offering in many activities such as transaction, payment, insurance agency, guarantee, securities brokerage and others. VDSC expected that fees from insurance and guarantees will have a notable contribution to the bank’s service income from 2018 onwards. For Vietcombank, services activities have been expanding with more cross selling of products. This will contribute more to the bank’s bottom line. VDSC forecast that service income growth will reach 30% in 2018 and 2019 for both ACB and Vietcombank.

BIDV, which is the bank with the lowest service income growth in VDSC’s coverage also has a plan to upgrade its core system in 2019-2020. As such, it is expected that service income growth can accelerate, though later than at other banks. This plan could put some pressure on the cost to income ratio.

Overall, in the near-term, VDSC believe that key generators of fee income growth include the settlement and insurance activities. In the long-term, excluding one-off income, it is expected that total service income of banks under the brokerage’s coverage will grow at a compound annual growth rate (CAGR) of 25.9% per year until 2022. VDSC also expected that the contribution of service income on TOI will be expanded from 8.6% (estimated in 2018) to 10.0% in 2019 and 13.8% in 2022.