English

English

Malaysia: Palm oil small caps reigning supreme

PETALING JAYA: Market sentiment seems to lean towards the larger, more established palm oil companies as being the greatest beneficiaries of the crude palm oil rally.

But the phenomenon in the stock market is rather peculiar because their share prices begged to differ.

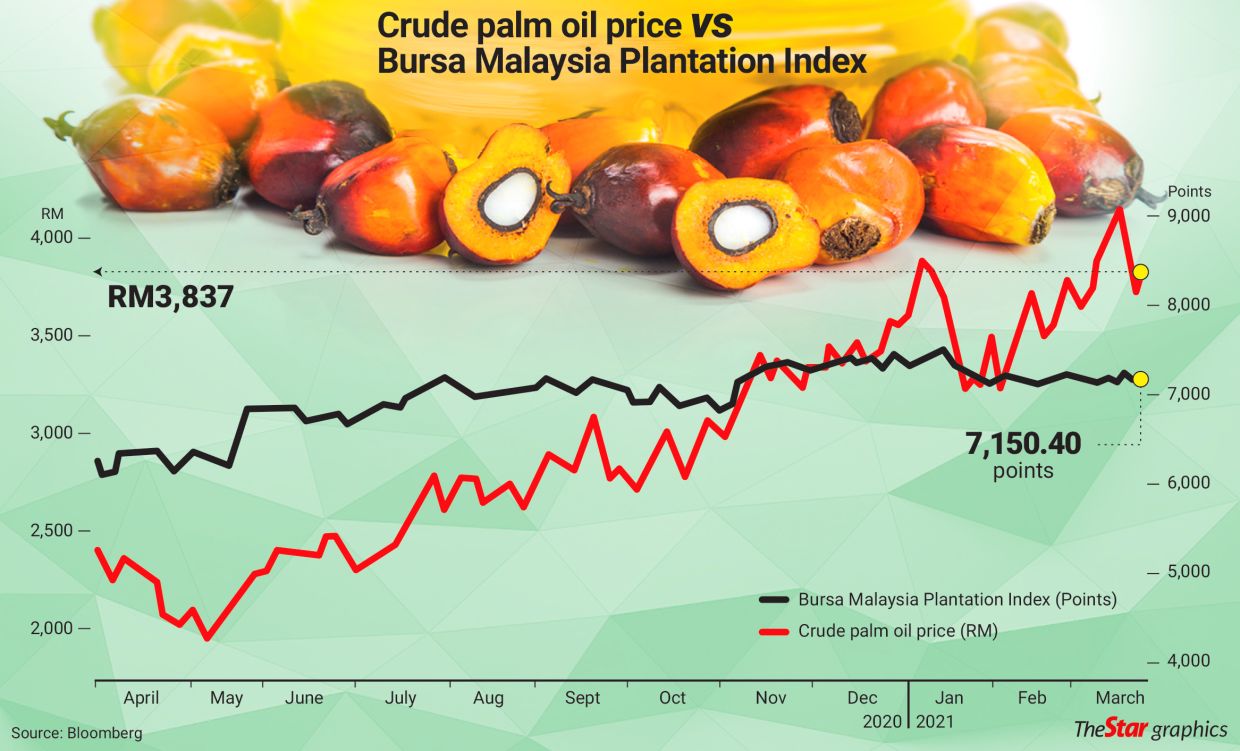

In fact, the small cap palm oil companies were the ones that have outperformed the larger brethren, from when the market bottomed out on March 19 last year and between the period when the crude palm oil price (CPO) touched RM3,000 in September last year and when it hit its stratospheric price above RM4,000 per tonne last week.

All 43 companies on the Bursa Malaysia Plantation Index are involved in the palm oil business, either as their main portfolio or one of their operating segments.

While the share prices have bounced off the bottom of March 19 a year ago, generally, most of their share prices have not been moving in tandem with the CPO price.

The price of CPO has risen some 40% since September but the Bursa Malaysia Plantation Index only inched up about 1%.

What seems to be a delay in the reaction on the share prices of palm oil companies has also sparked discussions in the market if the CPO price is sustainable.

From Sept 18 last year when CPO touched RM3,080 per tonne until March 15 when it hit its decade-high price of RM4,138,10 out of 17 companies in the billion dollar club or 58.82% saw their share prices advancing.

Even so, Far East Holdings Bhd was the best performer in this category, with a 22.84% increase to RM2.85.

was the best performer in this category, with a 22.84% increase to RM2.85.

The larger cap players such as Sime Darby Plantation Bhd and IOI Corp Bhd declined 2.58% and 5.36% respectively.

On the other end of the spectrum, out of 25 companies with a market capitalisation below RM1bil, 20 companies or 80% of them recorded an advancement in share prices.

Pinehill Pacific Bhd rose 81.25% to 58 sen. during the period. It is generally a loss-making company over the past several years except for its financial year ended June 2020, due to a one-off gain from the sales of its subsidiaries’ plantation assets.

TDM Bhd, which has also suffered losses in 2018 and 2019, rose 19.23% to 31 sen throughout the six-month period.

The small caps also dominated in terms of share price performances in their one-year period and year-to-date comparisons.

UOB Kay Hian head of research Vincent Khoo told StarBiz that even before the run up of CPO prices, that valuations of the large caps have always been well contained.

He added that fundamentally, the smaller palm oil players generally have better earnings leverage on the CPO price because it benefits the upstream players, most of whom are the small caps whereas the bigger companies were more exposed to downstream.

“There is always the concern that CPO prices may not sustain, which has been holding back a lot of funds from being too enthusiastic on Malaysian plantation stocks.

“But the fact that the CPO price has sustained much higher and much longer than expected, I think it’s a matter of time before the share prices start to react.

“The delay comes back to the issue of sustainability. If the CPO price sustains for a while and presumably if that would translate to a much better dividend, then I would assume that the interest would spill over to the sector, ” he said.

Rakuten Trade head of equity sales Vincent Lau said sentiment in the market on the sector was lukewarm due to the output, which has been impacted by the lack of workers, windfall profit levy and high taxes.

Explaining the possibilities behind the stronger rally of smaller caps against the bigger players, he said the retail participation in the stock market is still high, and the smaller caps may appeal more to them as compared to the better blue chips and better established companies.

“At the same time, the strong scrutiny on ESG practices could also be among the reasons, hence, funds and institutional investors are not moving into plantations, ” he said.

On the lack of reaction in share prices despite a strong CPO price catalyst, Lau said it may be due to the uncertainties revolving around the sustainability of the price.

“Even though output is currently lesser, the average selling price is now higher. The net effect will still be higher earnings for the industry players but somehow, it just doesn’t translate to interest in plantation stocks.

“There’s a delay in reaction to the share prices. It’s still lagging far behind the CPO price movement, ” Lau said.

Meanwhile, Khoo said he would not attribute the behavioural difference towards the large cap palm oil players due to the ESG spotlight, though it may be part of the reason why there was lesser participation from funds.

He said the greater concern was still the sustainability of CPO prices.

“If you look outside Malaysia, some large caps actually performed quite well and you can see better share price correlation whereas Malaysian counters are still trading sideways, ” he said.

An example is Singapore-listed Golden Agri-Resources Ltd, which has risen more than 50% over the past six months. It closed at 22 cents yesterday, giving it a market capitalisation of S$2.73bil (RM8.38bil).

Source: https://www.thestar.com.my/business/business-news/2021/03/23/palm-oil-small-caps-reigning-supreme