English

English

Singapore: Expenses incurred from working at home qualify for tax deductions

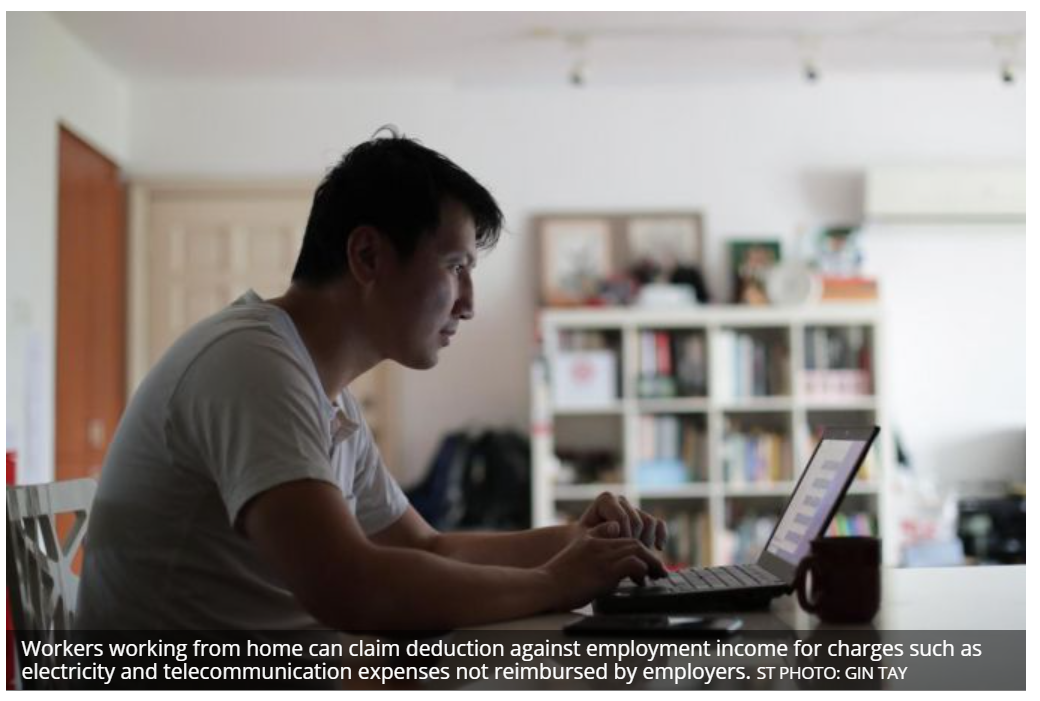

WORKERS working from home can claim deduction against employment income for charges such as electricity and telecommunication expenses not reimbursed by employers.

An Inland Revenue Authority of Singapore (Iras) spokesperson told The Business Times: “Tax deduction against employment income is allowable for expenses incurred wholly and exclusively in the production of employment income. “

To qualify for deduction, the expenses must be incurred while carrying out official duties, not reimbursed by the employer, and not capital or private in nature.

These expenses include the additional power and telecommunication bills incurred when employees are required to work from home. This is not limited to the “circuit breaker” period, the taxman said.

Companies started having employees work from home upon the urging of the Ministry of Manpower (MOM), especially during the circuit breaker period from April 7.

However, even when the circuit breaker was removed after June 1, the MOM has said that working from home should still be the default mode of working and businesses must adopt telecommuting to the maximum extent.

Iras said that for those who have incurred work-related charges this year may claim for a deduction against employment income in next year’s income tax filing. It also allows an equal apportionment basis among the working individuals in the same household, if there are more than one person working from home.

Senoko Energy reported an approximately 30 per cent increase in the average monthly electricity consumption in April for customers that use advanced meters, as compared to the January-February period.

Advanced meters allow electricity consumption to be measured at half-hourly intervals.

James Chong, head of commercial division at Senoko Energy, said: “While this is only reflective of a selected segment of our customer base, we expect to see a similar trend among our other residential customers, especially for families whose homes were unoccupied during office hours, pre-Covid.”

For most households, it is not exactly clear if consumption has gone up or by how much during the circuit breaker period, as they use meters that require manual reading.

A Keppel Electric spokesperson told BT that the Open Electricity Market retailer cannot comment on the usage of residential consumers for now. “Most customers are on manual meters and SP Services only takes meter reads every two months. With the circuit breaker, they have also suspended meter reading for April and May. We will only know the actual readings later.”

A Facebook post showed that SP Group’s meter readers would not be visiting households to record their utility usage during the circuit breaker period, so April, May and June bills would be estimated consumption.

The electricity tariffs before the goods and services tax decreased from 24.24 cents per kwh to 23.02 cents per kwh for the April to June quarter. This means that the average monthly electricity bill for a family living in a four-room Housing Board flat will decrease by S$3.89.

As it may be difficult for an employee to calculate the exact amount of the allowable expenses that have been incurred as a result of working at home, Iras will accept the difference in electricity and telephone bills before and after working from home.

For example, if the electricity bills before and after working from home are S$50 and S$60 respectively, the difference of S$10 can be claimed as deduction being expenses incurred for work purposes.

Where government rebates have been provided, taxpayers have to ascertain the portion of the electricity expenses incurred for work purposes based on the amount of charges net of government rebates.

As for broadband WiFi connection set up for work purposes, employees may claim the WiFi monthly subscription fees as a deduction. However, such one-time charges as installation or connection fee cannot be claimed because they are capital in nature.

Further, if WiFi has been set up before working from home, no deduction can be claimed for such expenses. To claim the expenses incurred for working from home, taxpayers must keep for five years proper records on these expenses and documents such as confirmation from the employer stating the period of working from home.

Source: https://www.businesstimes.com.sg/government-economy/expenses-incurred-from-working-at-home-qualify-for-tax-deductions?cx_testId=46&cx_testVariant=cx_2&cx_artPos=3#cxrecs_s