Thailand

Thailand

Singapore core inflation climbs to 5.3% in September; headline inflation steady at 7.5%

SINGAPORE’s core inflation rose further to 5.3 per cent in September but headline inflation held steady at 7.5 per cent, according to Department of Statistics consumer price index (CPI) data on Tuesday (Oct 25). Both readings were in line with economists’ expectations.

The pickup in core inflation was due to larger price increases for items such as food, services and retail and other goods. But headline inflation – which includes accommodation and private transport costs – remained the same as higher core and accommodation inflation were offset by lower private transport inflation.

The Monetary Authority of Singapore (MAS) and Ministry of Trade and Industry (MTI) maintained their full-year expectations for headline inflation at 6 per cent and core inflation at 4 per cent.

For 2023, headline and core inflation are still projected to average 5.5-6.5 per cent and 3.5-4.5 per cent respectively. Excluding the transitory effects of the goods and services tax (GST) hike next year, headline and core inflation are expected to come in at 4.5-5.5 per cent and 2.5-3.5 per cent respectively. (*see amendment note)

But MAS and MTI also noted upside risks to this outlook, “including from fresh shocks to global commodity prices and more persistent-than-expected external inflation”. They expect core inflation to stay elevated in the next few quarters before slowing in the second half of 2023 as domestic labour market tightness eases and global inflation moderates.

RHB senior economist Barnabas Gan, who maintained his full-year inflation forecasts, expects headline and core inflation momentum to decelerate towards the year-end as commodity price pressures dissipate. He sees core inflation still staying above the symbolic 2 per cent handle, with headline inflation easing to around 6 per cent.

Barclays economist Brian Tan reduced his 2022 headline inflation forecast to 6.2 per cent from 6.3 per cent, but raised his 2023 forecast to 5.6 per cent from 5.4 per cent. He expects headline inflation to moderate to 3.8 per cent by 2024.

He expects core inflation to be 4.2 per cent in both 2022 and 2023 – though the GST hike will likely raise this to a peak of 5.8 per cent in February 2023 – before moderating to 3.2 per cent in 2024.

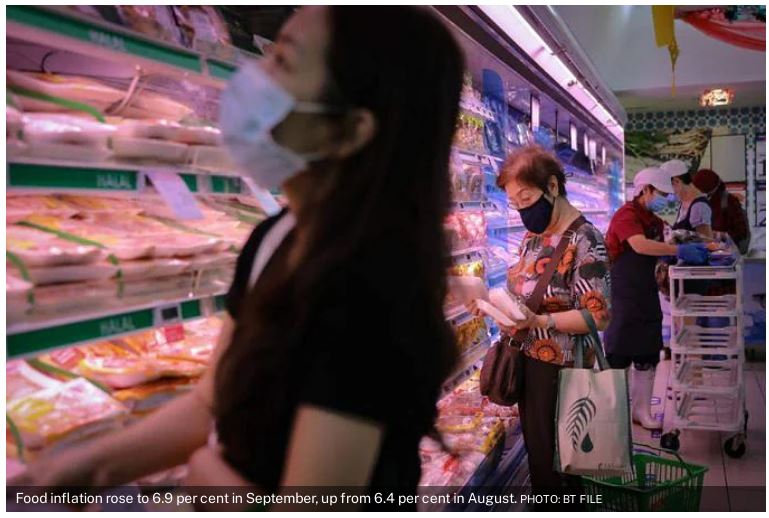

Food inflation rose to 6.9 per cent in September, up from 6.4 per cent in August. Inflation rates also rose for accommodation; services; and retail and other goods. Electricity and gas inflation stayed steady at 23.9 per cent.

But private transport inflation moderated to 22.3 per cent, slowing from 24. 1 per cent in August, due to a slower pace of increase in car and petrol prices.

On a month-on-month basis, core CPI and headline CPI increased by 0.5 per cent and 0.4 per cent respectively.

MAS and MTI expect imported inflation “to remain significant for some time”, while domestically, firms are expected to pass through rises in import, labour and other business costs to consumer prices “amid resilient demand”.

Maybank economists Chua Hak Bin and Lee Ju Ye noted that the wage-price spiral – when rising wage costs push companies to raise prices for consumers, which in turn leads workers to demand higher pay – may intensify in the coming quarters, as the Progressive Wage Model is expanded to cover food services, waste management and occupational sectors from March 1 of next year.

They also expect accommodation costs to continue rising, pushed up by returning non-resident workers, delays in property completion and possibly higher demand from property sellers going through the 15-month HDB wait out period.

UOB kept its headline and core inflation forecasts unchanged at 6 per cent and 4.2 per cent respectively. For 2023, they expect headline and core inflation to be 5 per cent and 4 per cent respectively, or 4 per cent and 3 per cent respectively if excluding the 2023 GST impact.

OCBC chief economist and head of treasury research and strategy Selena Ling noted that inflation is likely to remain an important consideration in the upcoming Budget 2023 and the next MAS policy meeting in April, “with more cost-of-living relief and further monetary policy tightening potentially still on the table”.

In April, Maybank’s Chua and Lee expect another upward re-centering of the Singapore dollar nominal effective exchange rate (S$NEER), similar to what the MAS did in October. Their model suggests that the S$NEER “is currently trading at about 1.1 per cent above the mid-point of the new re-centered band, with room left for further appreciation”.

RHB’s Gan instead expects the MAS to slightly steepen the S$NEER gradient by 0.5 per cent, while not changing its width and level at which it is centred.

Citi analyst Kit Wei Zheng is not ruling out an off-cycle move in January if Q4 data points to sufficiently large upside surprises to MAS’s forecasts.

“Historically, off-cycle moves were preceded by surprises of 40-50 basis points in the preceding quarter but the threshold could be lowered if MAS deems tightening needs to be front-loaded to further reduce risks of second round effects from the GST hike,” he said.

*Amendment note: An earlier version of this article incorrectly stated that excluding the transitory effects of the GST hike next year, headline inflation is expected to come in at 4.5-5.6 per cent. It is in fact 4.5-5.5 per cent. The article above has been revised to reflect this.

Source: https://www.businesstimes.com.sg/government-economy/mobile-spotlight/singapore-core-inflation-climbs-to-53-in-september-headline