Thailand

Thailand

New peak in Singapore private home prices expected by the end of 2018

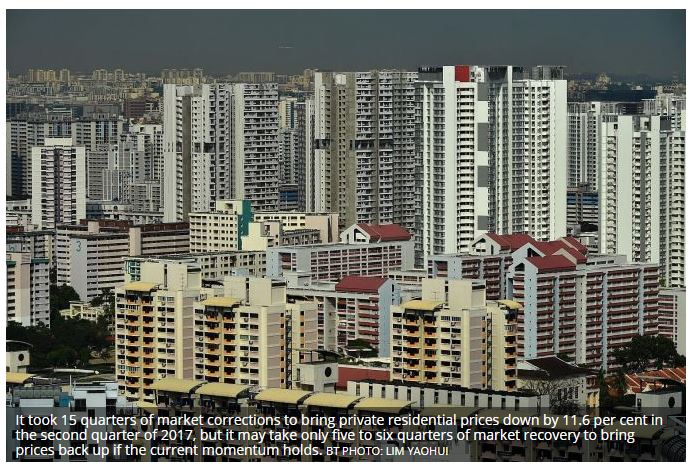

IT TOOK 15 quarters of market corrections to bring private residential prices down by 11.6 per cent in the second quarter of 2017, but it may take only five to six quarters of market recovery to bring prices back up if the current momentum holds.

Analysts are expecting a new peak in private home prices by the end of this year as developers roll out new launches on land they have acquired at significantly higher prices.

Flash estimates from the Urban Redevelopment Authority (URA) on Monday showed that private home prices rose for the fourth straight quarter, up 3.4 per cent in the second quarter after a 3.9 per cent increase in the first quarter.

This left the URA’s overall private residential price index at just 3.6 per cent below its last peak of Q3 2013 and 9.1 per cent above the last trough of Q2 2017; the price index for non-landed private homes in the second quarter this year is 1.7 per cent below the Q3 2013 peak based on the flash estimate.

In particular, non-landed home prices in the suburban region or Outside Central Region (OCR) are just 0.8 per cent shy of the last peak.

Cushman & Wakefield senior research director Christine Li said: “The sentiment is inching us towards another peak. Singapore property prices are likely to recover to the 2013 peak levels in one or two quarters.

OrangeTee & Tie head of research and consultancy Christine Sun said she expects Q3 2013 peak prices to be breached as early as in the third quarter of this year, barring any external shocks or government intervention.

“With many new launches in the pipeline, we expect private home prices to continue to trend upwards for all market segments for the next quarter, especially since many projects may be launching at new benchmark prices owing to the higher land costs,” Ms Sun added.

JLL national research director Ong Teck Hui noted that the second-quarter price increase was underpinned by more new launches with strong pricing as well as increased volume of transactions.

His caveats analysis showed transaction volume rose 14.2 per cent in the second quarter from the first quarter, with new sales volumes up 48 per cent while resale and sub-sale volume remained roughly flat. This was in tandem with more new project launches in the second quarter than in the quarter-ago period.

The rise was led by a 3.8 per cent jump in the prices of landed homes, followed by a 3.3 per cent uptick for non-landed homes.

“Landed prices had fallen more substantially than non-landed between 2013 and 2017 and its price increase during this recovery cycle has lagged non-landed properties,” Mr Ong observed. “As landed prices appear attractive, buyers have been drawn to the landed market contributing to the firmer price increase.”

In the non-landed segment, prices in the city-fringe or Rest of Central Region (RCR) jumped the most – by 5.7 per cent in the second quarter, after registering a 1.2 per cent uptick in the first quarter. Analysts note that this coincides with a jump in transaction volumes in the region, with bullish pricing at new launches such as Amber 45, Park Place Residences, Margaret Ville, The Verandah Residences and Harbour View Gardens.

Mr Ong estimates that transaction volume in the RCR rose 34.2 per cent in the second quarter, with new sales accounting for 45.8 per cent of its transaction volume, significantly higher than 31.7 per cent in the first quarter. The overall median price of S$1,665 per square foot (psf) was achieved in the RCR during the quarter, 12.7 per cent higher than that in the first quarter, based on caveats lodged.

Tricia Song, Colliers International head of research for Singapore, estimated that the median psf pricing at Amber 45, Park Place Residences and Margaret Ville in May were 13-25 per cent above comparables. Meanwhile, the resale market could have benefited from collective sales beneficiaries looking for a replacement home, she said.

But in the suburban or Outside Central Region (OCR), non-landed home prices may grow at a measured pace as the market digests the supply, Ms Song added.

URA’s second-quarter flash estimates show that non-landed private home prices rose 2.9 per cent in the suburban or Outside Central Region (OCR), and 1.4 per cent in the Core Central Region (CCR), after a respective 5.6 per cent and 5.5 per cent jump in the first quarter.

Ms Song is eyeing more upside for CCR non-landed prices in the coming quarters given the pipeline of new residential developments that could be launched. These include 3 Orchard By The Park, South Beach Residences, 8 St Thomas, and One Draycott.

Most analysts are expecting an 8-15 per cent jump in private home prices, with ZACD executive director Nicholas Mak being the most bullish with a forecast of 12-17 per cent. But they see government intervention as premature when an increase in launch supply and rising interest rates are under way.

“Policy risk will definitely be heightened but the government will monitor how the market will react to the upcoming new launches first,” said Knight Frank Singapore head of research Lee Nai Jia.

Mr Mak added: “Whether the residential property market recovery could continue for another one to two years would depend on several factors, such as the economy, job market, health of the HDB resale market and buying demand for new residential projects, which would be launched at record prices in their respective locations.”

Source: https://www.businesstimes.com.sg/real-estate/new-peak-in-singapore-private-home-prices-expected-by-the-end-of-2018