Thailand

Thailand

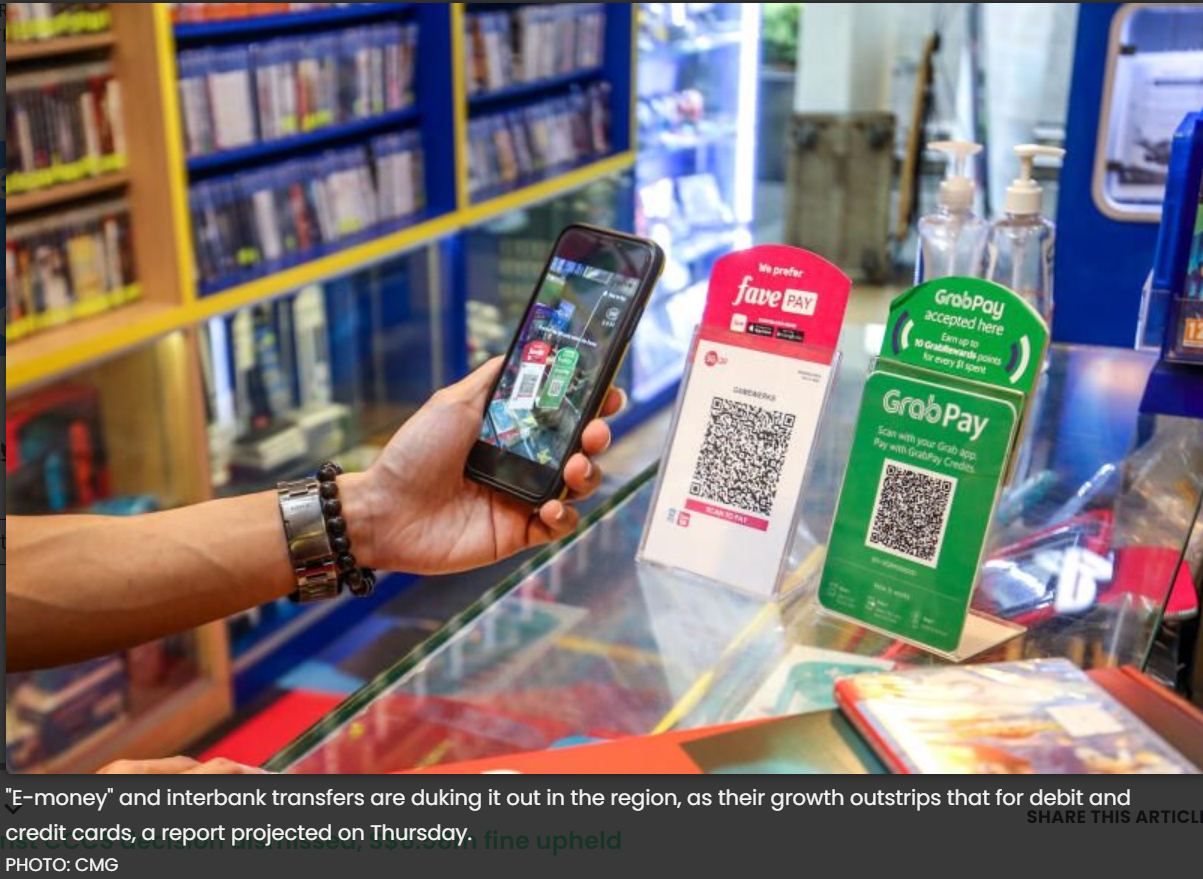

E-payments, fund transfers pip card transactions in South-east Asia

“E-MONEY” and interbank transfers are duking it out in the region, as their growth outstrips that for debit and credit cards, a report projected on Thursday.

Card payments declined in 2020, with transactions having shrunk as retail activity dimmed during Covid-19 and banks slowed card issuances.

Amid stiff competition, tech firms are now turning from digital money services to banking, said the report from S&P Global Market Intelligence analyst Sampath Sharma Nariyanuri.

These non-banks are expected to dominate the fintech scene in Indonesia and the Philippines, while incumbents stay solid in Singapore, Thailand and Malaysia. A slew of non-banks – especially e-wallet providers – either have more transaction value or are growing faster than banks in South-east Asia.

For instance, non-banks were behind 72 per cent of e-payment value in Thailand in 2019; in Malaysia, three non-banks together held the majority of the market share, the report noted.

Still, consumers in the more mature economies of Singapore, Malaysia and Thailand are tapping instant interbank transfers, such as PayNow, DuitNow and PromptPay.

“In Thailand and Singapore, e-money growth rates are trailing interbank payments,” said the report, noting that retail customers can continue to earn interest on bank deposits.

While fintechs could still get more access to bank payment infrastructure, the popularity of instant interbank payments “portends diminishing growth prospects for fintechs”.

In contrast, non-bank e-wallets have the most growth potential in cash-heavy Indonesia and the Philippines, where digital commerce penetration is low, the report suggested. Unbanked consumers in both markets are ditching banks’ traditional prepaid cards, and turning to e-wallets instead. For instance, S&P Global Market Intelligence estimated that 72 per cent of all e-money value in Indonesia was held in e-wallets in 2019.

And, although e-wallets are an attractive, less-regulated entry point for tech companies, large players are doubling down on other banking-related financial services, too.

“Grab, Sea Ltd and Ant Group are racing in South-east Asia to lock online shoppers into their ecosystems, which permeate nearly all activities of personal consumption,” the report said, citing the three firms’ recent digital banking licence wins in Singapore.

“With most other large economies in the region considering opening up the banking space to digital players, they are well-positioned to accelerate their pivot toward digital banking.”

For instance, Grab has rolled out a micro-investment service and e-commerce installment plans, and could offer personal loans from bank partners through its app.

All the same, the report warned that non-bank tech firms face losses in a crowded market, from limited revenues and high consumer and merchant acquisition costs.

It said: “While there are at least 256 non-bank e-money issuers, the digital payments landscape in the region will increasingly gravitate toward the large ecosystems.”

The S&P Global Market Intelligence report looked at retail payments on cards, interbank payments and stored-value wallet systems in South-east Asia’s five largest economies.

Source: https://www.businesstimes.com.sg/garage/e-payments-fund-transfers-pip-card-transactions-in-south-east-asia